The photovoltaic industry is currently navigating a path rife with contradictions. On one hand, it faces an industry "winter" characterized by overcapacity, price involution, and performance pressure on leading companies—the entire value ch

Technological Breakthrough: The Iterative Path of the PV Industry and China's Leadership

The photovoltaic industry is currently navigating a path rife with contradictions. On one hand, it faces an industry "winter" characterized by overcapacity, price involution, and performance pressure on leading companies—the entire value chain is under unprecedented operational strain. On the other hand, accelerated technological iteration, a blossoming of next-generation technology routes, and the long-term opportunities brought by the global energy transition have pushed industry attention to new heights. As P-type cell efficiencies peak, the N-type era officially begins. TOPCon solidifies its mainstream position, HJT and BC technologies are poised for takeoff, and perovskite and tandem technologies outline the future landscape. The core competition in the PV industry is shifting from scale expansion to technological innovation. Amid this wave of global energy transformation, China's PV sector, with its absolute industrial advantages, firmly holds the world's "leading" position. The judgments of industry authorities represented by Martin Green provide clear direction for the future technological trajectory and development path of the industry—only by achieving technological breakthroughs to navigate industry cycles can long-term dividends be captured in the global energy transition.

Industry "Winter": A Cyclical Correction, Not a Recession — Long-Term Demand Logic Remains Unchanged

The so-called "winter" in the PV industry is essentially a cyclical correction at a certain stage of industrial development, not a signal of industry decline. Since 2024, the PV industry has fallen into a supply-demand imbalance, with overcapacity across the entire chain reaching historical peaks. Polysilicon prices plummeted from a peak of 200,000 RMB/ton to 30,000 RMB/ton, and module minimum quotes dropped 40% compared to 2023. Industry leaders such as Longi Green Energy and Tongwei Co., Ltd. have successively reported expected losses. In 2024, the total losses of A-share PV listed companies exceeded 60 billion RMB, and operating pressure in the industry remained unabated in 2025. Rising prices of core raw materials like silver, intensified overseas trade barriers, and insufficient grid absorption capacity have further exacerbated the industry's involution. However, it is important to note that this "winter" did not stem from shrinking demand, but from capacity expansion far outpacing the pace of demand growth. In 2024, global newly installed PV capacity reached a historical peak of 553-601 GW. China, accounting for 61.24% of global new installations and ranking first globally for eleven consecutive years, became the core engine of global PV demand, also contributing 39.38% of global PV power generation. Even against the backdrop of slowing global demand growth in 2025, China's new PV installations maintained a high growth rate of 39.5%, with the coordinated development of large-scale centralized bases and distributed PV continuously providing demand support for the industry. It can be said that the short-term difficulties of the PV industry represent a "capacity digestion period" after rapid development, while the overarching trend of the global energy structure transitioning towards renewable energy determines that the industry's long-term upward logic has never changed.

Competing Technology Routes: TOPCon, HJT, BC, and Perovskite Outline the Future Landscape

The rapid adoption of TOPCon is not the endpoint of PV technology iteration, but the starting point of a new round of technological competition. The flourishing of multiple routes such as HJT and BC (back contact) technologies is pushing the PV industry into a new stage of parallel development.

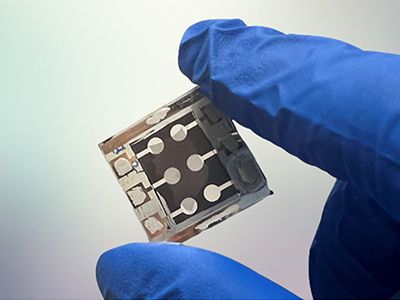

HJT (Heterojunction) Cells: High Theoretical Efficiency, Cost Remains a Bottleneck

HJT cells, with their core advantages of higher theoretical efficiency and lower degradation rates, have mass production efficiency expected to exceed 27%. However, issues such as high equipment investment costs and high silver paste consumption constrain their large-scale application speed. They are currently still in the industrial "tackling" stage of reducing costs and increasing efficiency.